The worldwide spread of COVID-19 that began in late 2019 triggered a catastrophic global economic shutdown, with businesses forced to close and millions of workers laid off. The Maldivian government has positioned themselves to meet the challenge of mitigating the spread of COVID-19 and recover from the economic downfall of the disease.

The frustrations due to the pandemic have caused the public to call out withdrawal from their pension funds. Economic Minister Fayyaz had reassured the public that it has not come to that level and it is important to secure pension funds for the future.

It is important to remember that pensions are a long term investment over time. It is the long-term savings plan for the future.

According to an expert on how pension funds work, the government should meet the requests of the public with additional and new relief loans or other arrangements. An alternative option, one without leaning towards withdrawal from pension funds.

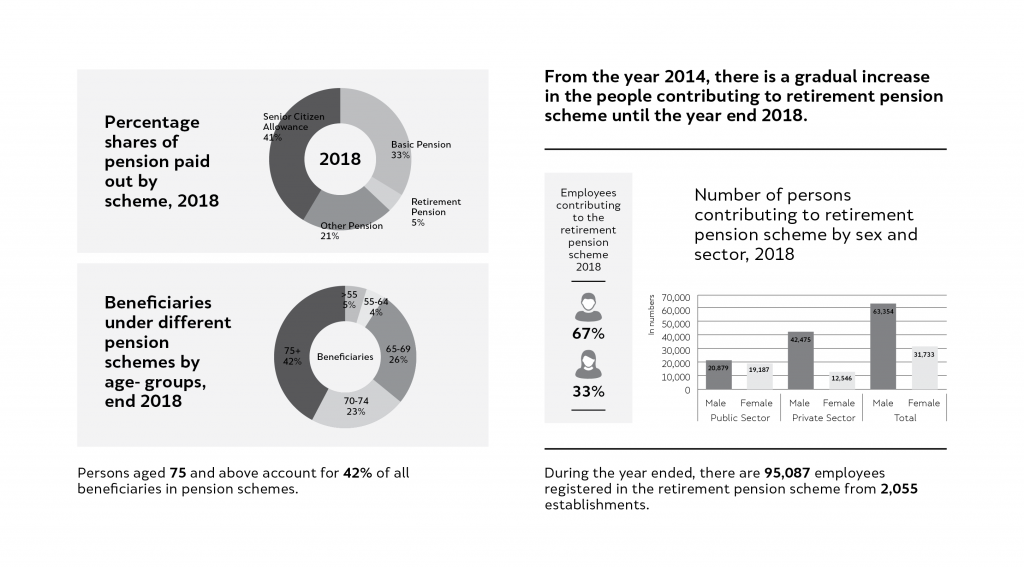

With the introduction of the Pension act in 2009, Maldives established a multi-tier pension system. The primary objective of the Maldives Retirement Pension Scheme (MRPS) is to ensure that individuals save during employment to cater for their livelihood in retirement.

Employees between 16 to 65 years of age and their employers are required to participate and pay contributions to MRPS. 7% respectively for the mandatory monthly contributions to the scheme. Foreign nationals and self-employed individuals working in the Maldives can participate in MRPS voluntarily

The money collected as pension contributions are not kept in cash, as a matter of fact, the Pension Office in the Maldives is obligated to find suitable investment options and transfer these funds collected as pension to best possible investment avenues.

Investing involves rules and procedures, hence, the money invested cannot be converted to cash as and when required. Some investments involve a deadline and in others, the proceeds received to play a major role when converting investments to cash.

Funds are also invested in with the objective to maximize pension savings. Early withdrawals can lead to the reduction of member savings and result in insufficient funds to provide a pension.

Although the value of MRPS Fund exceeds 13 billion, individual savings of some members are relatively low as contributions are tiered to the basic salary of employees. Early withdrawals can easily exhaust savings of such members in no time.

These funds have the potential to grow and provide a decent pension for the individuals in the longer run.

A professional banking industry individual had said that these pension funds have specific roles for each individual. Some may have plans to use it as the down payment for a house. If allowed the opportunity to withdraw, there might not be anything saved for the future.

Contributions to the scheme stops at the age of 65 years and members may start to draw down on the pension plan at this age. The amount is calculated by Balance in Retirement Savings Account / 14 years (168 months). The pension can also be used to secure housing loans and to perform the Hajj Pilgrimage.

Money in the pension funds is not liquidated funds. They are investments made. Liquidating the investments made before they mature will cause an economical setback.

Full details are available at the link below: